The markets appear to be a game of three halves at the moment. The US markets are resilient with equities holding their highs, Europe is gently slipping but the leader is currently China where equity markets have tanked over the past few days. To many, China has become the cradle of the next crisis. With little else going on in the world the amount of airtime and speculative attention that China is getting has already spilled into its secondary markets. Now whilst Australia may indeed be struggling with its own Dutch Disease the current China concerns are giving the Aussie bears more ammo to load up on positions that can only be described as "covering the table" - short AUD/USD, long EUR/AUD, short AUD/ZAR, BRL, CAD, you name it and the number of structured basket term sheets TMM are seeing relating to shorting Aussie are indicating Tabloid positioning. And we didn't even mention Copper or Chinese H-Shares. Yet much of this new wave is based upon China not paying top dollar for Australian commodities much longer.

The assumptions on China we will come back to in a minute, but the thing that strikes us most is the regionality of the opinions being expressed. US and leverage accounts are particularly negative on China and Australia, whereas Europe and real money accounts are more balanced. As usual though, the Chinese and Australian views remain overall pretty up beat on themselves. As ever TMM will try and explain this with a simple chart:

And it seems that even those with more optimistic views on China (Asia-based investors) have finally caught the "China is slowing sharply" bug and capitulated as February's export data (that TMM have already addressed here, concluding they weren't as bad as they seemed) and most recently the HSBC Flash PMI have provided new bear food, driven particularly by those in the US that view China as a Ponzi scheme. Now, TMM have mentioned before that they sit more in the middle of the two Jims (Chanos & O'Neill), neither of the opinion that China is to spectacularly crash nor become the world's growth engine (at least, not anytime soon). And they don't deny the fact that the banking system is full of NPLs related to the 2009-10 stimulus, and these will certainly be an overhang for the next couple of years. But that is in the price and, when considered upon the backdrop of being largely state owned & directed, TMM find it hard to get too excited about both the impact upon the economy more broadly - unlike in the West, loss-recognition and balance sheet repair (which would likely impede credit creation) are not exactly the priorities of either bank managements nor policymakers.

One thing that has puzzled many China-watchers has been the lack of expected policy easing in response to the weaker activity data and slowing inflation. The trouble is that Chinese data is very difficult to read, and TMM constantly receive somewhat, err, "lazy" analysis from both analysts and punters. A brief list of issues: (i) Lunar New Year plays havoc with January and February, and even can have an effect upon March due to the moving around and distortion of seasonal effects, (ii) the quality of the data is poor due to collection (and "massaging") issues, (iii) the data is not easy to understand as much of it arrives in "YoY Cumulative YTD" format, a relic of earlier central planning (see chart below of China Value Added of Industry YoY Cumulative YTD - a chart that is impossible to interpret in this form), (iv) seasonal adjustment factors have dynamically changed as China's economy has changed in composition over the past several years, and (v) there is an important difference between nominal and real figures (for example, the combined Jan/Feb nominal export growth of 7% was poor, but in real terms, was rather stronger than would have been expected given lagged US/EU orders). Any analysis of Chinese data is only complete when the above are considered - and most of the junk that both the Street & Blogosphere have pumped out on this neglect at least one of the above.

E.g. - What the heck does this mean?

So that's TMM's whinging out the way (and we profusely apologise for whinging at all!).

We digress. Reconstructing the above data, the below chart shows the YoY change in Value Added IP (purple line) and the 6m/6m seasonally adjusted annualised rate (saar, green line). The YoY rate is essentially flat, and while the economy clearly slowed in the latter half of 2011, the weakness appears exaggerated by base effects. The 6m/6m saar (green line), which is essentially a measure of growth momentum, clearly bottomed in December and has begun to move higher. The official China PMI also bottomed late last year (more on this below). Chinese policymakers observing the same data may well have come to the conclusion that easing is not really required - TMM would concur.

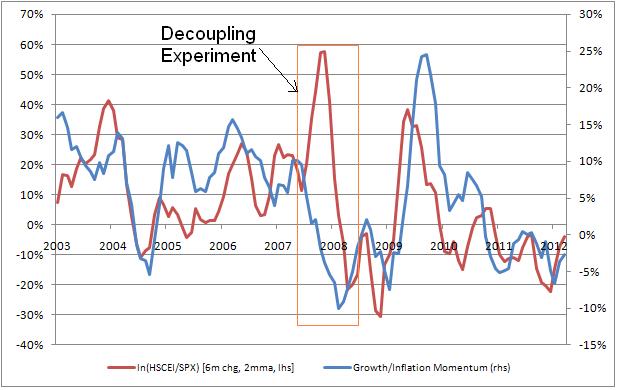

Of course, growth is only half the story - inflation is the other ingredient to the Growth/Inflation mix. But this too has fallen since the oil/food price-driven increase last year. Putting these together in a very simple model, there is a reasonable correlation between relative equity moves (see chart below, of the relative performance of Chinese H-Shares vs. SPX [Red line], vs. this naive metric [blue line]). No single driver can explain market moves, but broadly, TMM reckon that (as macro guys) the growth/inflation mix is a principal component. Obviously there are divergences related to the 2007-9 failed Decoupling Experiment, the world not being linear (and neither are returns) etc, but TMM think this is a useful way to think about China.

So, back to TMM's PMI model. This has reasonable error bounds that have caught them out before, functions of dynamic seasonal adjustments, but is nevertheless of some use at least. The top line model reckons a PMI of 52.7 - TMM are sceptical of this given the HSBC Flash PMI was so poor - but stripping out the seasonal produces 51.2, which is a smidge above consensus. TMM, however, are less concerned about the absolute level, and more about the direction. Specifically, should the number come out close to consensus, it would confirm that activity bottomed in December in line with the Value Added IP momentum above. A disappointment, on the other hand, would likely be met with eventual policy easing.

Putting all of the above together with bearish sentiment and interesting technicals in H-Shares (see below chart), TMM have begun building a long position both here and in AUD ahead of this weekend's PMI number, and would look to buy the dip into any knee-jerk sell-off should the number disappoint by only a tad. Again, the trouble here related to Lunar New Year and the other complicating factors mentioned above mean that the turn in momentum that TMM reckon is ongoing will not necessarily show up in the hard data for a couple of months. This is a risk TMM will have to take...

And with that, TMM brace themselves for a ravaging in the comments and wish their readers a profitable Q2.

No comments:

Post a Comment